Chinese Mainland Retail Market: Market Positioning of Hong Kong Sports Products

(Consumer Survey Results)

Key Findings

- The Chinese mainland has a huge e-commerce retail market, and the government has implemented various policies to facilitate cross-border e-commerce imports, allowing many sports products to benefit from preferential import tax and customs clearance conveniences through cross-border e-commerce channels. This provides relevant e-commerce businesses with numerous market development opportunities.

- Sports products are the second popular product category shopped online, with 56% of respondents saying they have bought sports products online. Additionally, 26% mentioned having bought Hong Kong sports products online. Consumers aged 30-49 are the most frequent online shoppers of these products. There are substantially more males buying sports products online than females.

- Consumers said that product quality and texture (35%) is the most important consideration when purchasing sports products online. For those who have bought Hong Kong sports products, the first consideration is brand image and word of mouth (37%). The considerations of consumers of different age groups are quite different. Male consumers give top consideration to product quality and texture, while female consumers consider customer service quality most important. The consideration factors of consumers from different locations are not identical.

- The average order value (AOV) for the online purchase of sports products is highest for tier-three city consumers (RMB2,656), followed by mainland GBA city consumers (RMB2,440). In buying Hong Kong sports products, the AOV of consumers from mainland GBA cities, tier-one cities and tier-three cities are lower, reaching respectively RMB2,068, RMB1,971 and RMB1,960.

- When buying sports products through online shopping platforms, consumers mainly obtain product information from official brand information channels, product reviews and online presenters. Consumers across several regions value official brand information channels most. Consumers from tier-one cities value product reviews, while those from mainland GBA cities give top consideration to the choice-product pages of e-commerce platforms. Consumers of all age groups consider official brand information channels most important. Female as well as male consumers value official brand information most.

- Mainland consumers mainly use comprehensive/shelf-based e-commerce platforms as their shopping channel, with over 90% of the respondents (accounting for 95% of the total) using these platforms for online shopping. When shopping for cross-border or imported products online, consumers generally prefer using Tmall Global and JD Worldwide, with 73% and 63% of the respondents reporting that they use these two platforms to buy overseas/cross-border/globally sourced products online.

In 2024, HKTDC Research commissioned a market survey agency to conduct a questionnaire survey of 2,200 middle-income class or above consumers from different mainland cities. The aim was to understand their online consumption habits and their preferences regarding Hong Kong products. For details, please refer to Hong Kong Businesses Navigating Chinese Mainland E-commerce Retail Market—Consumer Survey Results. |

Chinese mainland leads the global e-commerce retail market

The Chinese mainland e‑commerce market is leading globally and is huge in size. National Bureau of Statistics figures show that the Mainland’s online retail sales of physical goods surged by approximately 54.1% from RMB8.5 trillion in 2019 to RMB13.1 trillion in 2014. This accounted for 26.8% of the total retail sales of all consumer goods and is an important factor for the current sustained growth of the mainland consumer market. Furthermore, according to a report jointly published late last year by the HKTDC and the Hong Kong Export Credit Insurance Corporation [1], Hong Kong companies interviewed generally believe that the Chinese mainland e‑commerce market will hold the greatest growth potential in the coming two years.

The booming of the mainland online retail market is reflected not only in the steady growth in total sales but also in the diversification of product categories. Data from the Ministry of Commerce reveal that, in the first half of 2025, consumers were already very accustomed to buying various consumer goods through online channels. In the online retail sales of physical goods, sports and recreation supplies (4.67%) accounted for a sizeable market share.

Pay attention to legal and regulatory requirements in the e-commerce field

The Mainland government has introduced a number of laws and regulations targeting the e‑commerce industry to ensure its healthy development. In particular, since 1 January 2019, the E-commerce Law of the People’s Republic of China has been in force on the Mainland to regulate e‑commerce activities and maintain market order. In addition, sports product companies must pay attention to and comply with various legal and regulatory requirements related to the e‑commerce industry, including:

- Refunds and returns: According to the Law of the People’s Republic of China on the Protection of Consumer Rights and Interests, consumers making online purchases have the right to return goods within seven days without giving a reason.

- Personal information handling: The Measures for the Supervision and Administration of Online Trading [2] stipulates that online trading businesses that collect and use the personal information of consumers must adhere to the principles of legality, rationality and necessity; state explicitly the purposes, methods and scope of collection or use of information, and obtain the consent of consumers.

- Dos and don’ts in marketing: The Code of Conduct for Online Presenters [3] mandates that online presenters should guide users to interact civilly, express themselves rationally, spend reasonably, and must not hype hot social topics and sensitive issues, or intentionally create “hot issues” in public opinion.

- Anti-unfair competition practices: The newly revised Anti-unfair Competition Law of the People’s Republic of China [4] stipulates that platform operators are forbidden to use pricing rules to force or quasi-force vendors into selling commodities below costs, thereby disrupting market competition.

(For details, please refer to An Analysis of the Chinese Mainland’s E-commerce Retail Market [Research Report])

Regulations governing cross-border e-commerce imports

If Hong Kong companies choose to expand into the mainland market by importing products through cross‑border e‑commerce, they must comply with a series of regulatory requirements related to product imports. The Mainland also implements relevant preferential measures for cross‑border e‑commerce imports, including:

- Taxation: Cross-border e-commerce imports are eligible for preferential taxation treatments, including zero tariff within quota for goods on the retail import list and the levying of import value-added tax (VAT) and consumption tax at 70% of the statutory tax payable.

- Product specifications: Cross-border e-commerce imports can enjoy more simplified customs clearance procedures than general trade. This means that cross-border e-commerce retail imports need not go through first-time import licensing, registration or record-filing requirements and will only be subject to regulations for the importation of personal-use articles. Nevertheless, goods imported through cross-border e-commerce retail channels can only be sold directly to consumers and cannot be resold.

- Product scope: The Mainland maintains a List of Imported Goods in Cross-border E-commerce Retail. Only coded commodity items on this list are eligible for being imported into the Mainland through cross-border e-commerce, and commodities outside this list will have to be imported through ordinary trading means. Hong Kong companies must ensure that their products are in compliance with the latest commodity category revisions before proceeding with importing and selling through cross-border e-commerce channels.

- Purchase limit: Mainland consumers purchasing imported commodities through cross-border e-commerce retail are subject to a single transaction limit of RMB5,000 and an annual transaction limit of RMB26,000.

(For details, please refer to An Analysis of the Chinese Mainland’s E-commerce Retail Market [Research Report])

Mainland consumers shop online frequently

In the second and third quarters of 2024, HKTDC Research commissioned a market survey agency to conduct a questionnaire survey of mainland online shopping consumers. The survey findings reveal that mainland consumers shop online frequently. Overall, the respondents shop online 9.4 times a month on average.

Regionally, in tier‑one cities and mainland GBA cities where economic development is higher and logistics infrastructure better, consumers have higher monthly online shopping frequencies than those in other regions, averaging 11.7 and 11 times per month respectively.

Efficient Logistics Services: products received in 3.2 days after ordering on average

Currently, mainland online shopping consumers can usually take delivery of their products soon after placing orders on online platforms. The survey shows that, on average, the consumers interviewed can receive their products within 3.2 days after ordering. In particular, consumers in tier‑two and tier‑three cities can take delivery soonest, getting their online purchased products in an average of 3.1 days. Males can get their products sooner than females: in 3.0 days on average. Consumers in the 18‑29 and 30‑49 age groups can take delivery 3.1 days after ordering, which is earlier than for consumers aged 50 and above.

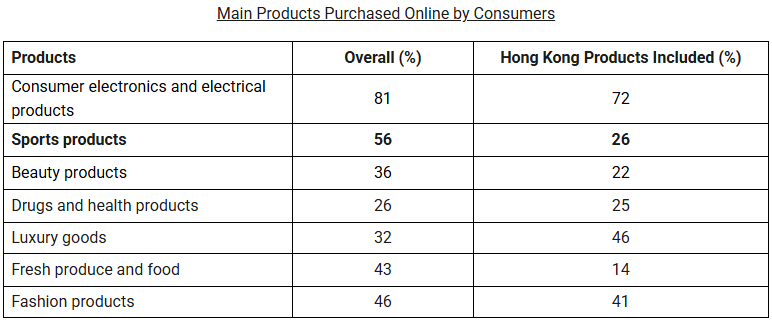

Sports products popular with online shoppers

Mainland consumers purchase all kinds of products from online platforms, with sports products ranking second in popularity among all product categories. For online shopping consumers of Hong Kong products, sports products are less popular. The survey findings show that, over the past year, 56% of the respondents reported buying sports products online, and 26% said they had bought Hong Kong sports products online.

Characteristics of online sports product purchases

- Highest proportion of sports product purchases in tier-one cities

Regionally, consumers in tier‑one cities have the highest proportion of online sports product purchases (63%), followed by mainland GBA cities (61%). In tier‑three cities, the proportion is 59%, and the proportion in tier‑two cities is 54%. The proportion in tiers four and five cities is only 42%.

Across regions, the trends of consumers shopping online for Hong Kong sports products vary appreciably, and the proportion of consumers shopping online for Hong Kong products is significantly lower than the overall proportion. The proportion of tier‑three city consumers purchasing Hong Kong sports products online is highest (37%). The proportions in tier‑one cities (26%) and mainland GBA cities (26%) are identical, followed closely by the proportion in tier‑two cities (24%), while the proportion in tiers four and five cities is only 21%.

- Consumers aged 30-49 shop online for sports products most frequently

In terms of age, consumers aged 30‑49 shop online for sports products most frequently (64%), followed by those in the 18‑29 age group (62%). Consumers aged 50 and above have the lowest frequency at only 36%.

Hong Kong sports products are most popular with consumers aged 18‑29 (33%), followed by consumers aged 30‑49 (24%). 23% of consumers aged 50 and above have shopped online for Hong Kong sports products.

- Males shop sports products online significantly more often than females

Gender‑wise, males (60%) buy sports products more frequently than females (52%). When it comes to buying Hong Kong sports products online, the proportion of male online shoppers (29%) is also higher than that for females (24%).

Considerations in shopping for sports products online

- Top considerations: product quality, product functions, customer service quality

When shopping for sports products online, mainland consumers pay most attention to product quality and texture (35%), product functions and specs (34%) and customer service quality (34%).

When buying Hong Kong sports products online, they give top consideration to brand image and word of mouth (37%), followed by product quality (34%) and price and availability of promotional discounts (34%).

- Considerations vary across regions

From a regional perspective, GBA consumers pay most attention to product quality (41%) and product functions and specs (40%), but they value additional fees (32%) and product design (32%) more than customer service quality (24%). Tier‑one city consumers pay more attention to product quality and texture (47%), followed by product functions and specs (42%), but they value brand image and word of mouth (36%) more than customer service quality (25%).

Tier‑two city consumers attach top importance to the quality of customer service (42%), followed by product quality and texture (41%), as well as price and the availability of promotional discounts (41%). To tier‑three city consumers, however, additional fees are their top consideration (39%), followed by price functions and specs (37%) and customer service quality (35%). Product quality (21%), on the contrary, is not among their top three considerations. Tiers four and five city consumers also give top consideration to additional fees (37%) when shopping for sports products online, followed by price and promotional discounts (32%), as well as return policy and efficiency (32%).

When buying Hong Kong sports products online, GBA consumers give top consideration to product functions and specs (46%) rather than brand image (30%), followed by additional fees (41%) and product design (41%). Tier‑one city consumers value product functions and specs most (50%), followed by product quality and texture (45%) and brand image (39%).

When buying Hong Kong sports products online, tier‑two city consumers pay most attention to price and availability of promotional discounts (50%), followed by customer service quality (43%) as well as product quality and texture (36%). Tier‑three city consumers, on the other hand, pay top consideration to product functions and specs (37%) as well as customer service quality (37%), followed by brand image (35%), additional fees (35%) and product design (35%). The considerations of tiers four and five city consumers are quite different to the overall considerations. They pay top attention to return policy and efficiency (47%), followed by brand image (44%) and then by product quality (41%) and additional fees (41%).

")

- Considerations of consumers in different age groups are different

In terms of age, when shopping for sports products online, the most important consideration for consumers aged 18‑29, irrespective of whether they are from Hong Kong, the Mainland or other areas, is brand image and word of mouth(42%), followed by price and promotional offers(34%) and additional fees (34%).

When consumers aged 30‑49 shop for sports products online, their most important consideration is product quality and texture (43%), followed by product functions (34%), and then by product image (32%) and promotional discounts (32%). In shopping for Hong Kong sports products online, their top consideration is brand image (38%), followed by product quality and texture (36%) and promotional discounts (36%).

The consideration factors of consumers aged 50 and above are significantly different. They pay less attention to brand in shopping for sports products online. Instead, they value customer service quality most (40%), followed by product functions and specs (35%). When shopping for Hong Kong sports products online, they give top consideration to return policy and efficiency (47%), followed by additional fees (41%), and then by product quality (35%), product functions and specs (35%) and customer service quality (35%).

- Males first consider product quality, females value customer service quality

By gender, when shopping for sports products online, male consumers give top consideration to product quality and texture, while female consumers pay attention to customer service quality. Male consumers pay most attention to product quality and texture (39%), followed by product functions and specs (34%), brand image and word of mouth (34%) as well as price and promotional discounts (34%). When shopping for Hong Kong sports products online, their priorities are different: they value brand image and word of mouth most (40%), followed by product quality and texture (36%), and then by price and availability of promotional discounts (33%).

On the other hand, female consumers give top consideration to customer service quality (41%), followed by product functions and specs (34%), and then by brand image (32%) and additional fees (32%). When shopping for Hong Kong sports products online, their top concerns are price and availability of promotional discounts (36%) and additional fees (36%), followed by product functions and specs (34%).

")

Value of Hong Kong orders

- Average order exceeds RMB2,000

Respondents spend as much as RMB2,090 per order on average when buying sports products online. When Hong Kong products are included, the average order is similar at RMB1,829.

- Spending highest in tier-three cities

By location, average spending on sports products is highest among respondents in tier‑three cities (RMB2,656), followed by consumers in mainland GBA cities (RMB2,440) and then by those in tiers four and five cities (RMB1,951).

- Hong Kong products depress spending in multiple locations

When Hong Kong products are included in the online shopping of sports products, respondents’ average spending is lower in tier‑two cities (RMB1,546), tier‑three cities (RMB1,960), tiers four and five cities (RMB1,651) and mainland GBA cities (RMB2,068). It is only in tier‑one cities that the average spending is higher (RMB1,971).

Promotion channels

- Official brand information channels most important

Overall, consumers mainly obtain information from official brand information channels (27%). They may also refer to product reviews (24%) and online presenters (23%).

When Hong Kong products are included, the channels through which consumers obtain information are basically the same as the overall picture: they mainly obtain information from official brand information channels (34%), and refer to product reviews and online presenters (22%). Hong Kong consumers will also pay attention to the information channels of retail stores and speciality stores (22%).

- Official brand information channels most important in multiple locations

Classified by location, consumers in tier‑two cities consider official brand information channels as most important (28%), followed by online presenters (27%), and then by product reviews (26%). When Hong Kong products are included, consumers in tier‑two cities value official brand information channels most (50%), followed by the choice‑product pages of e‑commerce platforms (25%) and then by online presenters (21%).

Consumers in tier‑three cities also consider official brand information channels most important (28%), followed by the choice‑product pages of e‑commerce platforms (23%), and then by retail store information channels (20%). When Hong Kong products are included, consumers in tier‑three cities consider official brand information channels as most important (30%), followed by product reviews (22%) and retail store information channels (22%).

Consumers in tiers four and five cities consider official brand information channels most important (26%), followed by retail store information channels (25%) and then by promotion by online presenters (24%). When Hong Kong products are included, consumers in tiers four and five cities consider promotion by online presenters as most important (34%), followed by official brand information channels (19%), product reviews (19%) and retail store information channels (19%).

Consumers in tier‑one cities, on the other hand, consider product reviews as most important (31%), followed by official brand information channels (28%) and the choice‑product pages of e‑commerce platforms (28%). When Hong Kong products are included, they consider official brand information channels as most important (39%), followed by retail store information channels (34%) and then by product reviews (27%).

To consumers in mainland GBA cities, the choice‑product pages of e‑commerce platforms are considered most important (28%), followed by official brand information channels (26%) and product reviews (26%). When Hong Kong products are included, they consider official brand information channels as most important (41%), followed by the choice‑product pages of e‑commerce platforms (24%) and then by product reviews (22%) and retail store information channels (22%).

")

Classified by age, consumers aged 18‑29 consider official brand information channels as most important (28%), followed by promotion of online presenters (24%) and then by retail store information channels (23%). When Hong Kong products are included, consumers aged 18‑29 are basically consistent with the overall considerations, with official brand information channels (34%) as the most important consideration, followed by retail store information channels (32%) and then by promotion of online presenters (24%).

Consumers aged 30‑49 also consider official brand information channels as most important (30%), followed by product reviews (26%) and then by online presenters (25%). When Hong Kong products are included, consumers in this age group mainly obtain information from official brand channels (38%), followed by the choice‑product pages of e‑commerce platforms (26%) and then by product reviews (23%).

Consumers aged 50 and above consider official brand information channels (22%) and product reviews (22%) as most important, followed by retail store information channels (20%). When Hong Kong products are included, consumers aged 50 and above have different priorities: they consider product reviews (29%) as most important, followed by official brand information channels (27%) and the choice‑product pages of e‑commerce platforms (24%).

- Both female and male consumers value official brand information most

In terms of gender, male consumers consider official brand information channels as most important (29%), followed by product reviews (24%), online presenters (24%) and the choice‑product pages of e‑commerce platforms (24%). When Hong Kong products are included, the considerations of male consumers are roughly the same, with official brand information (35%) as most important, followed by product reviews (25%) and then by online presenters (20%) and the choice‑product pages of e‑commerce platforms (20%).

Female consumers also consider official brand information channels (26%) as most important, followed by product reviews (24%) and then promotion by online presenters (21%) and retail store information channels (21%). When Hong Kong products are included, female consumers also consider official brand information channels (33%) as most important, followed by retail store information channels (31%) and then online presenters (24%).

")

Comprehensive e-commerce platforms as main online shopping channel

Mainland consumers mainly carry out online shopping on traditional comprehensive platforms. More than 90% of the respondents (accounting for 95% of the total) have used comprehensive/digital shelf e‑commerce platforms for online shopping, a percentage far higher than other platforms, such as live‑streaming/short video platforms (38%) and group buying platforms (32%).

In terms of regional distribution, over 90% of consumers across all regions primarily shop online via general merchandise/shelf‑based e‑commerce platforms, significantly higher than the second‑choice live‑streaming/short‑video platforms. Similarly, shelf‑based platforms are the primary online shopping choice for consumers across all age groups (each exceeding 90%). Regarding gender distribution, both men and women primarily shop on the same types of platforms, which are, in order: general merchandise/shelf‑based platforms, live‑streaming/short‑video platforms, and group‑buying platforms.

On the other hand, when shopping for overseas/cross‑border/global products. Consumers generally prefer using Tmall Global (73%) or JD Worldwide (63%). Classified by region, preferences for different platforms are also quite consistent, with consumers in all locations mainly choosing Tmall Global. In terms of age and gender, consumers’ preferences coincide. They mainly choose Tmall Global.

")

For sample details, please refer to Hong Kong Businesses Navigating Chinese Mainland E-commerce Retail Market - Consumer Survey Results

Related articles:

Chinese Mainland E-Commerce Retail Market: Market Positioning of Hong Kong Luxury Items

Chinese Mainland E-Commerce Retail Market: Market Positioning of Hong Kong Fresh Produce and Food

Chinese Mainland E-Commerce Retail Market: Market Positioning of Hong Kong Fashion Products

[1] For more details, please see Unleashing the Lucrative Potential of Cross-Border E-Commerce for Hong Kong Traders (Company Survey and Expert Opinion).

[2] For more details, please see Measures for Supervision of Online Transactions Take Effect in May.

[3] For more details, please see China Announces Code of Conduct for Online Presenters.

[4] For more details, please see Revised Anti-Unfair Competition Law to Take Effect on 15 October.

Original article published in https://hkmb.hktdc.com