Greece

Greece

GDP (US$ Billion)

257.07 (2018)

World Ranking 52/193

GDP Per Capita (US$)

24,716 (2018)

World Ranking 44/192

Economic Structure

(in terms of GDP composition, 2019)

External Trade (% of GDP)

74.4 (2019)

Currency (Period Average)

Euro

0.89per US$ (2019)

Political System

Unitary multiparty republic

Sources: CIA World Factbook, Encyclopædia Britannica, IMF, Pew Research Center, United Nations, World Bank

Overview

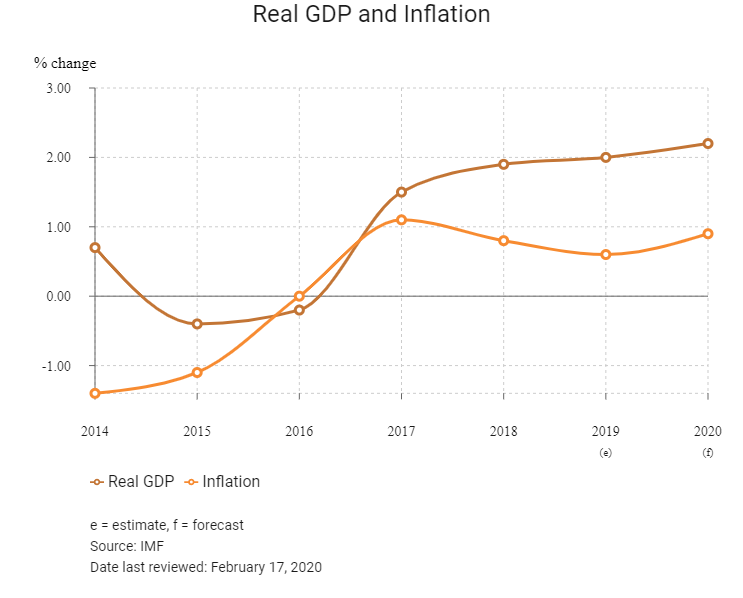

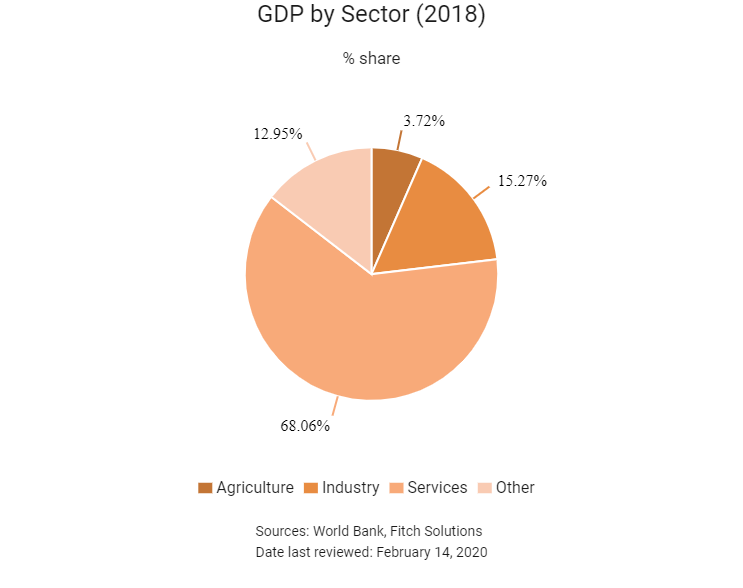

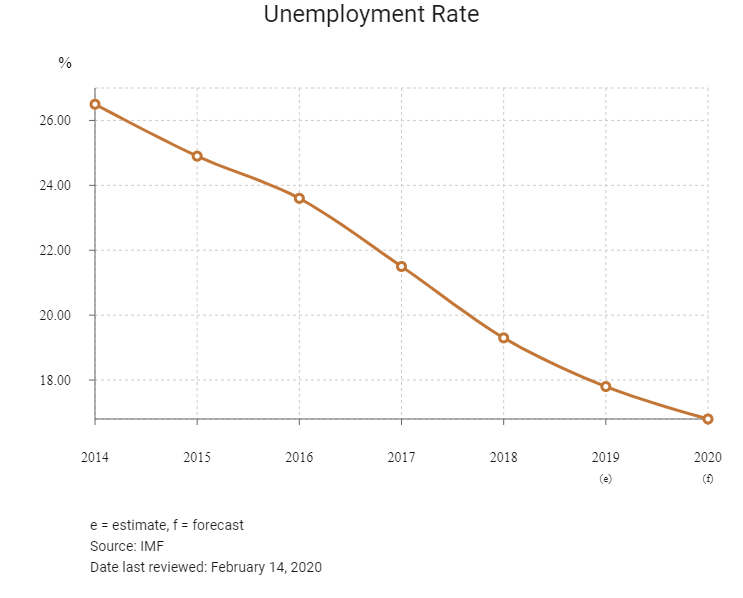

Greece is a high-income economy reliant on trade, tourism and the wider services economy – tourism, for example, accounts for about a fifth of Greece’s GDP. However, following the 2007-2008 global economic crisis, Greece’s economy deteriorated significantly. The government has adopted since 2010 several austerity programs that include cutting government spending, reducing the size of the public sector, decreasing tax evasion, reforming the healthcare and pension systems, and improving competitiveness through structural reforms to the labour and product markets. Greece has received substantial financial and technical support from its eurozone partners and the IMF over the past decade, geared towards fiscal sustainability and balance, public sector reorganisation and optimisation, and deficit reduction. This aid program is still in progress, while the heavy austerity measures add on to risks stemming from rising unemployment (and particularly youth unemployment), still-high debt load, austerity measures and general demographic decline. On the upside the announcement of a European Investment Bank initiative to fund infrastructure investment in Greece is set to provide broad support for the country’s construction sector as it continues to recover from a prolonged recessionary period.

Sources: Fitch Solutions, World Bank

Major Economic/Political Events and Upcoming Elections

January 2015

Elections were held to determine the 300 seats in the Voulí ton Ellínon (the Hellenic Legislature). SYRIZA’s Alexis Tsipras was tasked with creating a government following his party’s ability to win the greatest number of seats. SYRIXA formed a coalition with ANEL, allowing for Tsipras to be sworn in as Prime Minister.

September 2015

Legislative elections held after Tsipras resigns from post. The governing SYRIZA party won a near majority of seats in the Voulí ton Ellínon (the Hellenic Legislature) and formed a government with the Independent Greeks, allowing Alexis Tsipras to resume his role as Prime Minister.

June 2018

Greece and Macedonia sign an agreement to bring a 27-year long dispute over Macedonia’s name to an end. The country was to be named North Macedonia.

July 2019

Legislative elections were held, with the New Democracy party securing a majority 158 seats in the 300 seat parliament. Kyriakos Mitsotakis became Prime Minister on July 8, 2019.

January 2020

The European Investment Bank (EIB) approved a EUR180 million, 28-year loan to the government of Greece for the construction of the new Heraklion International Airport in Kasteli on Crete island. The EUR517 million project would also include construction of a new 18km motorway and a 6km access road. The new airport would replace the current airport serving Heraklion, which would be closed. Construction of the new airport was scheduled to be completed in five years.

Sources: BBC Country Profile – Timeline, national sources, Fitch Solutions

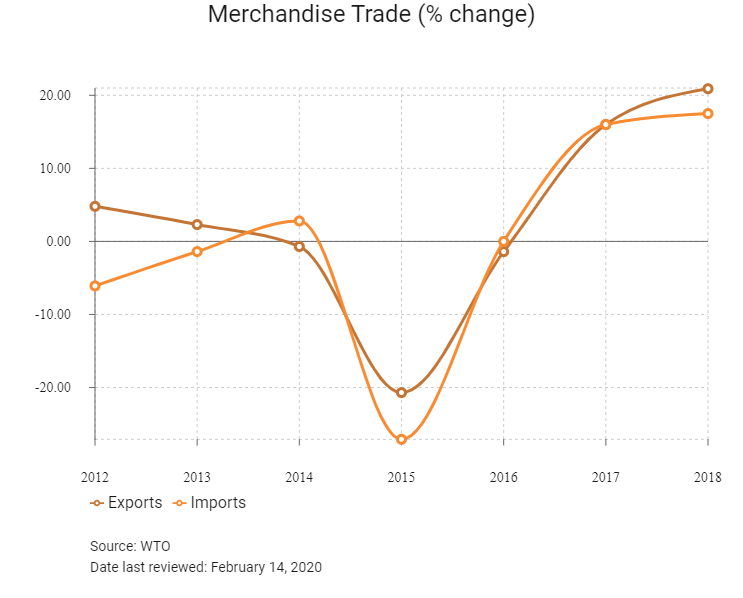

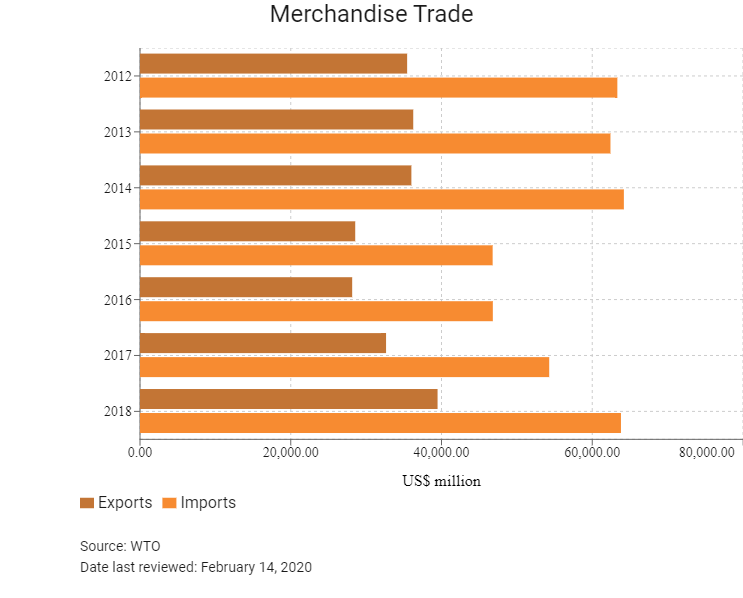

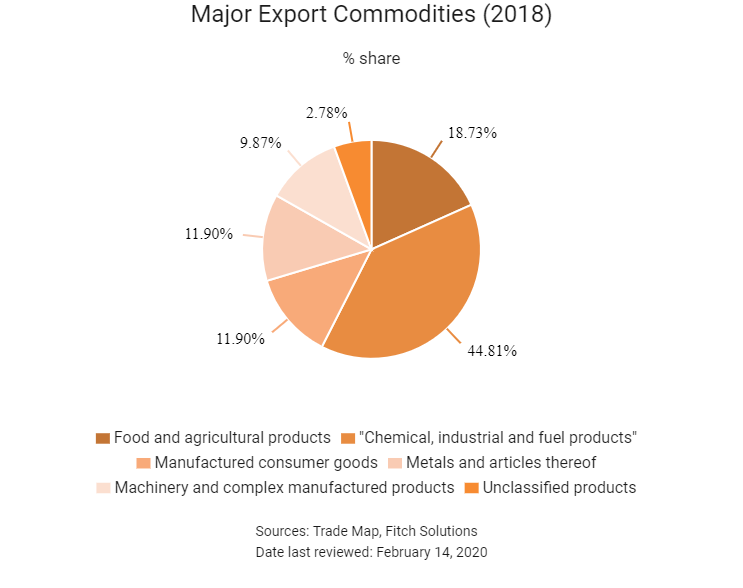

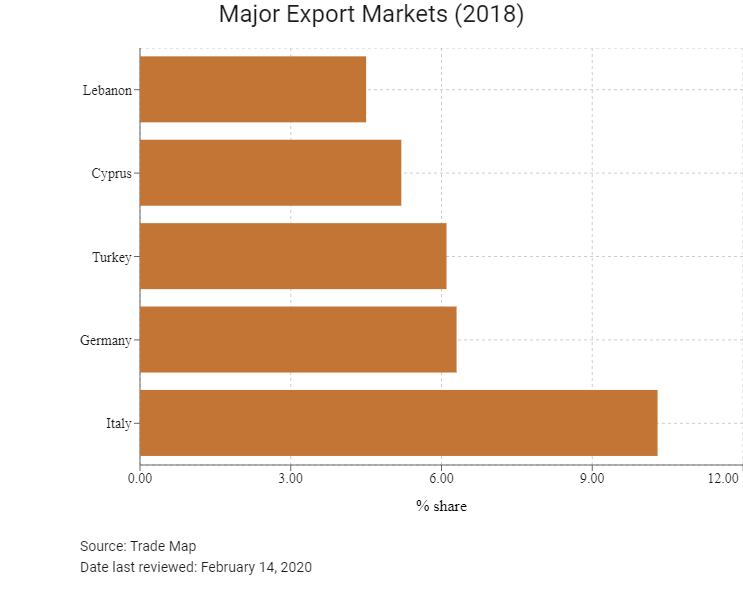

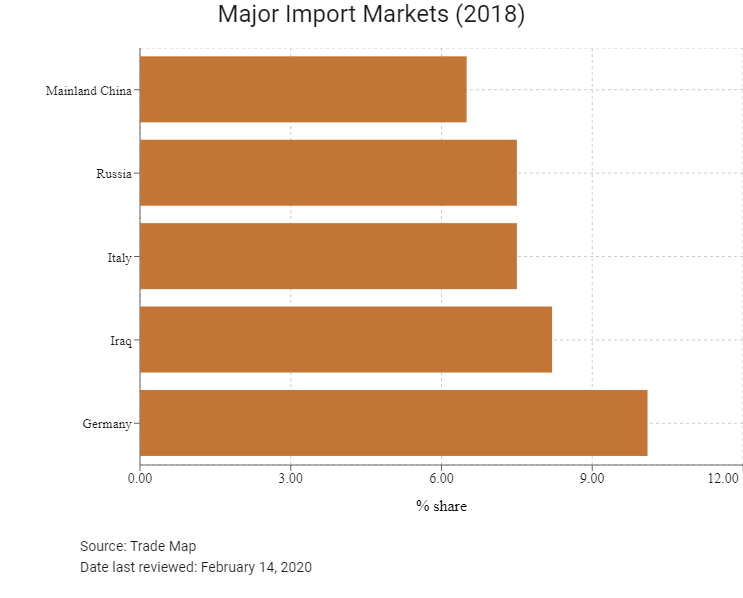

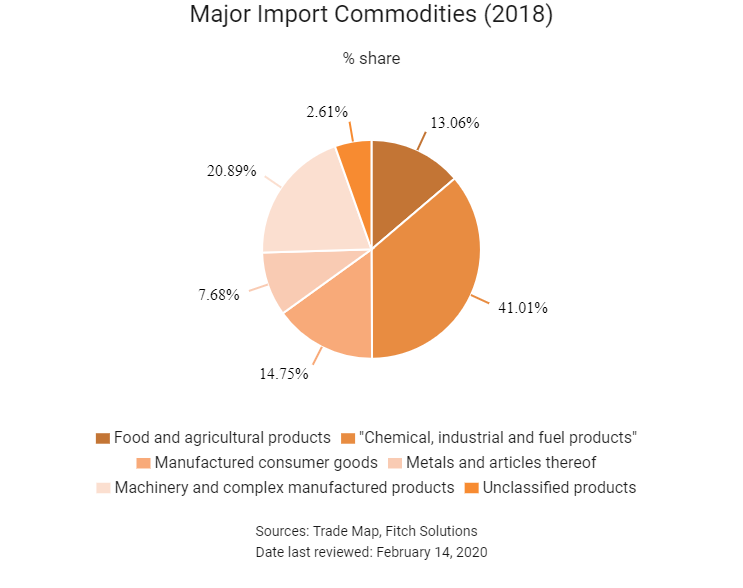

Merchandise Trade

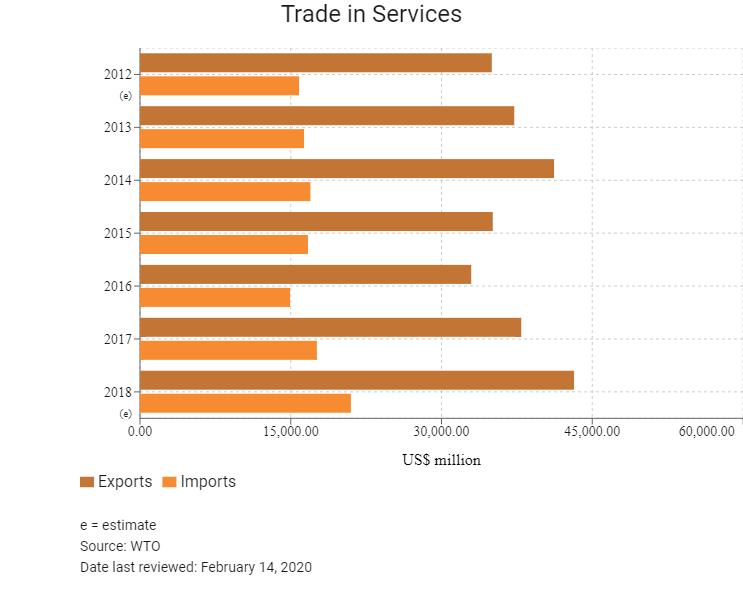

Trade in Services

- Greece has been a WTO member since January 1, 1995 and a member of GATT since March, 1950. The country is also a member of the European Union (EU) (since 1981), having adopted the euro in 2001.

- Greece applies the EU's Common External Tariff, which means goods manufactured and imported from within the EU are not subject to customs charges. The average tariff rate for EU states is just 1.57%, which is among the lowest globally. The duties for non-European countries are also relatively low, especially for manufactured goods (4.2% on average). However, textile, clothing items (high duties and quota system) and food-processing industry sectors (average duties of 17.3% and numerous tariff quotas) still see protective measures. Most of the country's major trade partners are within the EU, hence risks are less pronounced.

- The EU has imposed various anti-dumping measures on a wide range of products. As of Q319, the EU and EC apply anti-dumping duties on 52 product categories, affecting 15 states. The EU imposes anti-dumping duties on 30 categories of products from Mainland China and a few other Asian nations, predominantly in the areas of textiles, parts, steel, iron and machinery.

- In 2016, the EC introduced an import licensing regime for steel products exceeding 2.5 tonnes. The regulation will be active until May 15, 2020.

- On January 1, 2017, the EU imposed additional import duties on certain fruit and vegetables if the quantity of the goods exceeds the trigger volume level within the specified application period. As of January 2019, the EC has applied additional import duties on certain fruit and vegetables from Brazil, Israel, South Africa, Peru, Morocco, Egypt, India, Chile and Argentina.

- 73 countries have tariffs products affected by EU and/or EC tariffs; 631 products exported by Mainland China have tariffs placed upon them; 18 products exported by Hong Kong have EU tariffs placed upon them as of Q319.

- The EU imposes import quotas on rice imports from Cambodia, India, United States, Pakistan and Thailand.

- Beyond trade financing and loans, Greece does not implement any additional trade-related measures.

Source: WTO – Trade Policy Review, Fitch Solutions

Multinational Trade Agreements

Active

- The EU Common Market: The transfer of capital, goods, services and labour between member nations enjoy free movement. The common market extends to the 28 member nations of the EU, namely: Austria, Belgium, Bulgaria, Croatia, Cyprus, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden and the United Kingdom.

- European Economic Area-European Free Trade Association (Iceland, Liechtenstein, Norway and Switzerland): While it enhances trade flows between these countries and the EU, only Switzerland is a fairly major trading partner.

- EU-Turkey: The customs union within the EU provides tariff-free access to the European market for Turkey, benefitting both exporters and importers.

- EU-Japan Economic Partnership Agreement: In July 2018, the EU and Japan signed a trade deal that promises to eliminate 99% of tariffs that cost businesses in the EU and Japan nearly EUR1 billion annually. According to the EC, the EU-Japan Economic Partnership Agreement (EPA) will create a trade zone covering 600 million people and nearly a third of global GDP. The result of four years of negotiation, the EPA was finalised in late 2017 and came into force on February 1, 2019 after the EU Parliament ratified the agreement in December 2018. The total trade volume of goods and services between the EU and Japan is an estimated EUR86 billion. The key parts of the agreement will cut duties on a wide range of agricultural products and it seeks to open up services markets, particularly financial services, e-commerce, telecommunications and transport. Japan is the EU's second biggest trading partner in Asia after Mainland China. EU exports to Japan are dominated by motor vehicles, machinery, pharmaceuticals, optical and medical instruments, and electrical machinery.

- EU-SADC Economic Partnership Agreement (Botswana, Lesotho, Mozambique, Namibia, South Africa and Swaziland): An agreement between EU and SADC delegations was reached in 2016 and is fully operational for SADC members following the ratification of the agreement by Mozambique. The remaining six members of SADC not included in the deal (the Democratic Republic of the Congo, Madagascar, Malawi, Mauritius, Zambia and Zimbabwe) are seeking economic partnership agreements with the EU as part of other trading blocs – such as with East or Central African communities.

Provisionally Active

- The Comprehensive Economic and Trade Agreement (CETA): The CETA is an agreement between the (EU) and Canada. CETA was signed in October 2016 and ratified by the Canadian House of Commons and EU Parliament in February 2017. However, as of July 2019, the agreement has not been ratified by every European state and has only provisionally entered into force. The following EU countries have ratified CETA, making the agreement provisionally active for these states: Austria, Czech Republic, Denmark, Estonia, Spain, the UK, Croatia, Lithuania, Latvia, Malta, Portugal, Sweden and Finland. CETA is expected to strengthen trade ties between the two regions, having come into effect in 2016. Some 98% of trade between Canada and the EU will be duty free under CETA. The agreement is expected to boost trade between partners by more than 20%. CETA also opens up government procurement. Canadian companies will be able to bid on opportunities at all levels of the EU government procurement market and vice versa. CETA means that Canadian provinces, territories and municipalities are opening their procurement to foreign entities for the first time, albeit with some limitations regarding energy utilities and public transport.

- EU-Central America Association Agreement (Guatemala, El Salvador, Honduras, Nicaragua, Costa Rica, Panama, Belize and the Dominican Republic): An agreement between the parties was reached in 2012 and is awaiting ratification (29 of the 34 parties have ratified the agreement as of July 2019). The agreement has been provisionally applied since 2013, with the agreement being provisionally implanted among signatories.

Ratification Pending

- EU-Singapore FTA (EUSFTA): On February 13, 2019, the European Parliament passed the agreement which would see the creation of the EUSFTA. However, before the agreement is implemented, all the states involved will need to ratify the agreement through their individual legislatures; in this case, the FTA may become provisionally active along the lines of states which have already ratified the agreement.

- EU-Vietnam FTA: In July 2018, the EU and Vietnam agreed on final texts for the EU-Vietnam Free Trade Agreement (FTA) and the EU-Vietnam Investment Protection Agreement (IPA). On June 30, 2019, the relevant parties signed the agreement on both the trade agreement and the investment protection agreement. The signed agreements will be presented to both the EU and Vietnamese parliaments, as well as the individual parliaments of EU members, for ratification.

- EU-MERCOSUR FTA: After 19 and a half years, a deal to establish the FTA was agreed upon on June 28, 2019. The signed agreements will be presented to the parliaments of the affected states (EU and MERCOSUR members), as well as to the EU Parliament, for ratification before coming into effect. MERCOSUR consists of Argentina, Brazil, Paraguay and Uruguay (Venezuela’s membership has been suspended).

Under Negotiation

- EU-Australia: The EU, Australia's second largest trade partner, has launched negotiations for a comprehensive trade agreement with Australia. Bilateral trade in goods between the two partners has risen steadily in recent years, reaching almost EUR48 billion in 2017, and bilateral trade in services added an additional EUR27 billion. The negotiations aim to remove trade barriers, streamline standards and put European companies exporting to or doing business in Australia on equal footing with those from countries that have signed up to the Trans-Pacific Partnership or other trade agreements with Australia. The Council of the EU authorised opening negotiations for a trade agreement between the EU and Australia on May 22, 2018.

- EU-United States (Trans-Atlantic Trade and Investment Partnership): This agreement was expected to increase trade and services, but it is unlikely to pass under the Trump administration in the United States against the backdrop of rising global trade tensions.

Source: WTO Regional Trade Agreements Database, Fitch Solutions

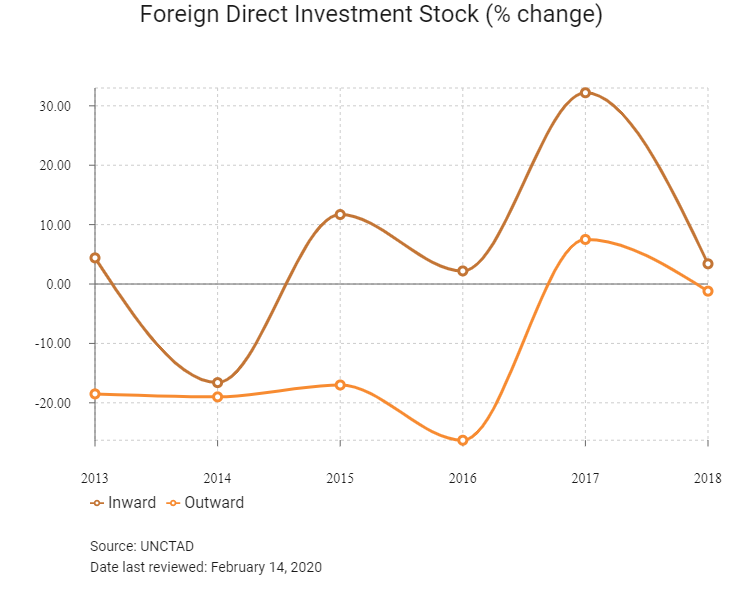

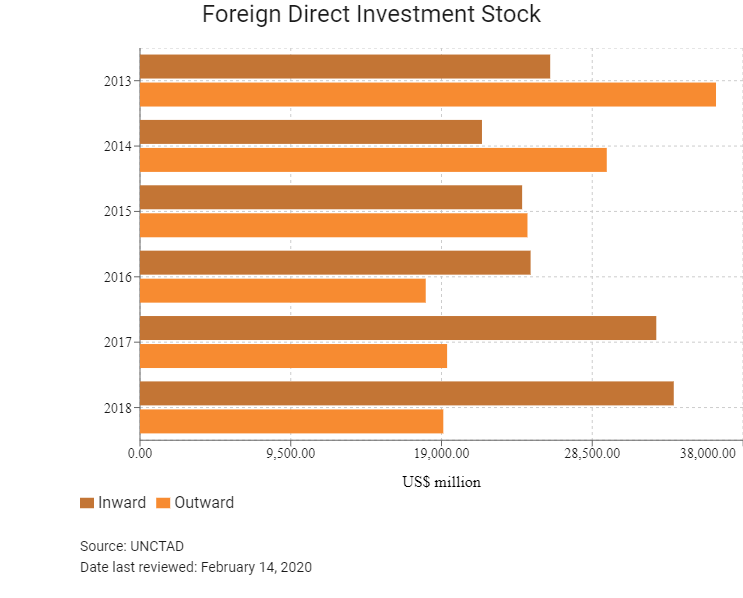

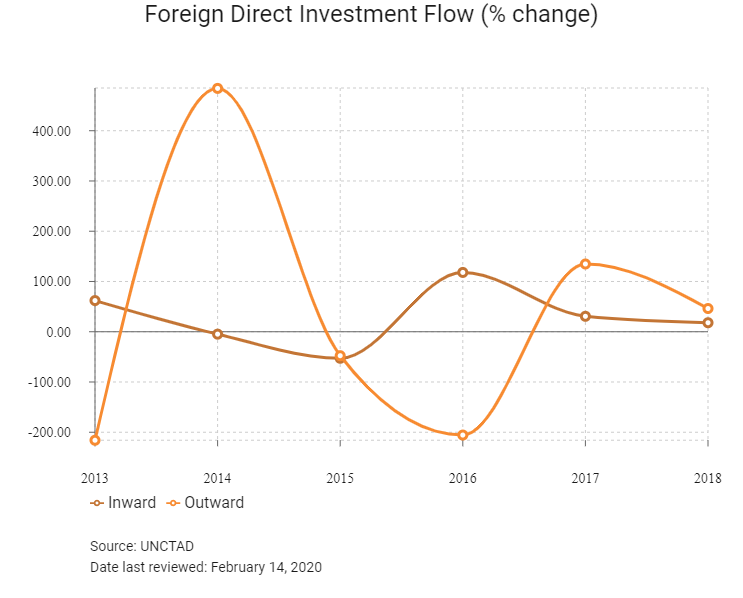

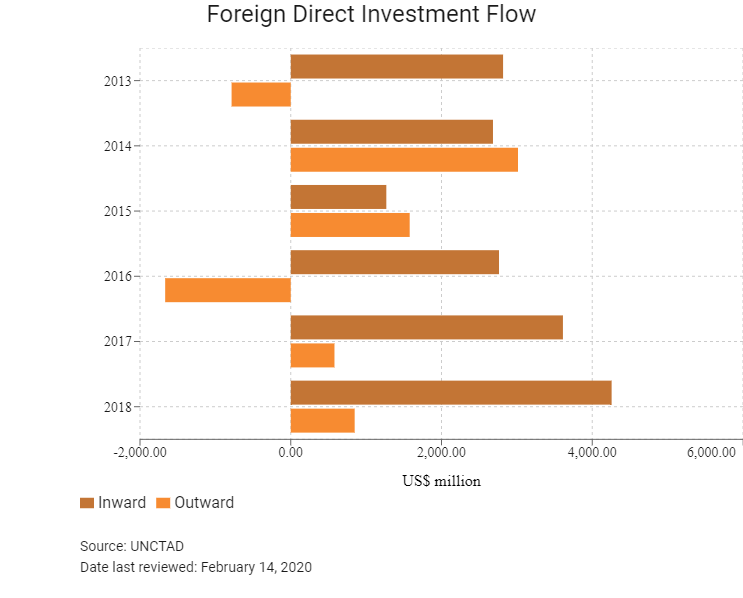

Foreign Direct Investment

Foreign Direct Investment Policy

- ‘Enterprise Greece’ is the Greek state’s investment and business facilitating agency, operating under the auspices of the Greek Ministry of Economy and Development. Enterprise Greece seeks to promote the country as an investment destination, especially in key sectors such as tourism, energy, food and agriculture, logistics, ICT, environmental management, and life sciences.

- According to the World Bank’s Doing Business report in 2020, Greece made starting a business easier by reducing the time to register a company with the commercial registry and removing the requirement to obtain a tax clearance.

- Greece imposes some restrictions on the foreign ownership or occupation of real estate. Non-EU entities or actors wishing to purchase real estate can request that the restriction is lifted via a petition which states the purpose of the property’s use.

- There are no minimum capital requirements for foreign investments into Greece.

- The recent announcement of a green infrastructure initiative in Greece via a partnership between the EIB and the National Bank of Greece will support opportunities across renewable energy, water infrastructure and enhancing energy efficiency. With EUR450 million available for financing, the infrastructure ‘fund of funds’ seeks to unlock an additional EUR200 million from other Greek banks by combining its financial resources and technical expertise to lower risk for other investors. In line with broader EU objectives, the partnership aims to focus on green projects, such as wind and solar parks, biomass and biogas plants and the construction of energy-efficient buildings; all of which would provide upside for our outlook for Greek project activity. In particular, support for the renewable energy sector aims boost activity that has been constrained previously by connectivity issues in the transmission grid network.

- Investments into industry, energy, tourism, transport, telecommunications, health services, waste management, and technology may be expedited if one of the following conditions are met:

- The investment exceeds EUR100 million

- The investment exceeds EUR15 million in industrial zones

- The investment exceeds EUR3 million and is part of the JESSICA Holding Fund (Joint European Support for Sustainable Investment in City Areas)

- The investment exceeds EUR40 million and creates at least 120 jobs

- The investment exceeds EUR5 million to be used for developing a business park

- Creates 150 new jobs or leads to the retention of 600 employees

- Under Greek law, credit institutions are allowed to approve the execution of transfers abroad up to EUR4,000 per customer in a two-month span.

- Businesses and investors are able to draw upon the International Chamber of Commerce and the International Center for Settlement of Investment Disputes in instances where arbitration is needed.

- There has been no expropriations of land or property in Greece over the country’s recent history. Although this does not exclude the possibility, it would make any such actions highly irregular.

- Greece is party to 46 active bilateral investment treaties, including one with Mainland China. An additional four treaties have been signed, but are not in force.

- The EU has in place 56 active Treaties with Investment Provisions with entities such as:

- MERCOSUR

- Association of South-East Asian Nations (ASEAN)

- Central American Common Market (CACM)

- Caribbean Community (CARICOM)

- Economic Community of West African States (ECOWAS)

- Gulf Cooperation Community (GCC)

- Southern African Development Community (SADC)

- Common Market For East And Southern Africa (COMESA)

- East African Community (EAC)

- West African Economic and Monetary Union (WAEMU)

- African Union (AU)

- Mainland China and Macau

Sources: WTO – Trade Policy Review, Fitch Solutions

Free Trade Zones and Investment Incentives

Free Trade Zone/Incentive Programme | Main Incentives Available |

| Job enhancement incentive | Under certain conditions, an increase by 50% and up to 14 times the minimum wage of an unmarried employee over 25 years old per employment of the employers’ contributions is provided. |

| General state aid for machinery and equipment | Tax exemption (up to the maximum state aid available within regional state aid limits) for the purchase and installation of new and used machinery (given that the machinery is no older than seven years old), as well as for the purchase of vehicles for on-site use. |

| State aid for large investments | The relevant party can benefit from: - A fixed corporate income tax rate for 12 years (pursuant of the completion of the investment plan) OR - Tax exemptions equal to 10% of eligible expenditure, capped at EUR5 million May also benefit from a ‘fast track’ procedure for processing and receiving licenses and permits. |

| General state aid for new independent SMEs | Applicable for enterprises that are being established or that have been established within seven years of submitting their application for the investment. Tax exemptions and cash grants available for: - Investment in tangible and intangible assets - Estimated wage costs arising from the creation of jobs as a result of an initial investment - Studies and consultancy services - Start-up costs - Energy efficiency costs - High-efficiency cogeneration costs - Investment costs for the production of energy from renewable energy sources - Energy efficient district heating and cooling |

| State aid for innovative SMEs | Tax exemptions and cash grants (of up to 70% of the maximum for a state) for: - Investment costs in tangible and intangible assets - Estimated wage costs arising from job creation, as a result of an initial investment, calculated over a period of two years - Studies and consultancy services - Start-up costs - Energy efficiency costs - Investment costs for the production of energy from renewable energy sources |

| State aid for synergies and networking | Applies to clusters of at least six enterprises in the Attika region and Thessaloniki prefecture, or of at least four enterprises in all other regions that are formed under a legal entity (additional requirements exist). Tax exemptions, cash grants and leasing subsidies: - Investment costs in tangible and intangible assets - Estimated wage costs arising from job creation as a result of an initial investment, calculated over a period of two years - Innovation clusters costs |

Sources: US Department of Commerce, Fitch Solutions

- Value Added Tax: 24%

- Corporate Income Tax: 24%

Source: aade.gr

Important Updates to Taxation Information

- For business income earned in tax years 2019 and onwards, corporate income tax is reduced to 24% (from 28%). The same corporate income tax rate may also apply to institutions which have not opted for the special provisions pertaining to deferred tax.

- For dividends distributed as of January 1 2020, the dividends tax rate is reduced from 10% to 5%.

- As of June 1, 2019, the social security contributions owed by employers has been reduced to 24.81% (from 25.06% prior). Employees will pay 15.75%, down from 16%.

- The corporate income tax rate has been reduced to 28% from 29%. The lower rate is applicable to accounting periods after January 1, 2019. The corporate income tax rate will drop by 100 basis points every year until it reaches 25% in 2022.

Business Taxes

Type of Tax | Tax Rate and Base |

| CIT | 24% |

| Value Added Tax | - Standard rate : 24% - Reduced rate: 13% - Super-reduced rate: 6% |

| Withholding Tax: royalties | 20% |

| Withholding Tax: dividends | 5% |

| Withholding Tax: interest | 15% |

| Real Estate Transfer Tax (RETT) | 3.09% (flat rate) |

| Payroll Tax | Progressive tax ranging from 22% to 45% |

| Social security contributions | - 24.81% by the employer - 15.75% by employee |

Source: aade.gr

Date last reviewed: February 14, 2020

Work Permit

EU member citizens do not require a work permit, but their employer must inform the job office about their employment. Citizens of the EEA (with EU member states, Iceland, Norway and Lichtenstein) and Switzerland do not require a visa to enter, reside and work in the country.

No work permit is needed by foreigners from outside the EU if they have a permanent residence or family reunion permit, have been granted asylum, study in the country or have blue or green cards.

Obtaining Foreign Worker Permits

Individuals from non-EU countries require residence and work permits. The procedure to be granted a work permit includes a review of the local job market to ensure that there is no Finnish or EU job seekers available to fulfil the position. Employers must first apply for a permit to hire foreign workers. The vacant position must be reported to the local district Labour Office and cannot be changed at a later stage to fit the profile of a potential employee. The candidate must then apply for a work permit. The government issues the permit for a maximum of two years, which can be repeatedly prolonged, but always for a maximum of two years, and may be renewed as many times as needed. The permit process takes an average of one month.

Blue Card

Intended for the stay of a highly qualified employee. A foreigner holding a blue card may reside in the country and work in the job for which the blue card was issued, or change that job under the conditions defined. High qualification means a duly completed university education or higher professional education which has lasted for at least three years. The blue card is issued with the term of validity three months longer than the term for which the employment contract has been concluded, but for the maximum period of two years. The blue card can be extended. One of the conditions for issuing the blue card is a wage criterion – the employment contract must contain gross monthly or yearly wage at least at the rate of 1.5 multiple of the gross average annual wage.

Sources: Europa.eu, Fitch Solutions

Sovereign Credit Ratings

Rating (Outlook) | Rating Date | |

| Moody's | B1 (Stable) | 01/03/2019 |

| Standard & Poor's | BB- (Positive) | 25/10/2019 |

| Fitch Ratings | BB (Positive) | 24/01/2020 |

Sources: Moody's, Standard & Poor's, Fitch Ratings, Reuters

Competitiveness and Efficiency Indicators

World Ranking | |||

2018 | 2019 | 2020 | |

| Ease of Doing Business Index | 67/190 | 72/190 | 79/190 |

| Ease of Paying Taxes Index | 65/190 | 65/190 | 72/190 |

| Logistics Performance Index | 42/160 | N/A | N/A |

| Corruption Perception Index | 67/180 | 60/180 | N/A |

| IMD World Competitiveness | 57/63 | 58/63 | N/A |

Sources: World Bank, Transparency International

Fitch Solutions Risk Indices

World Ranking | |||

2018 | 2019 | 2020 | |

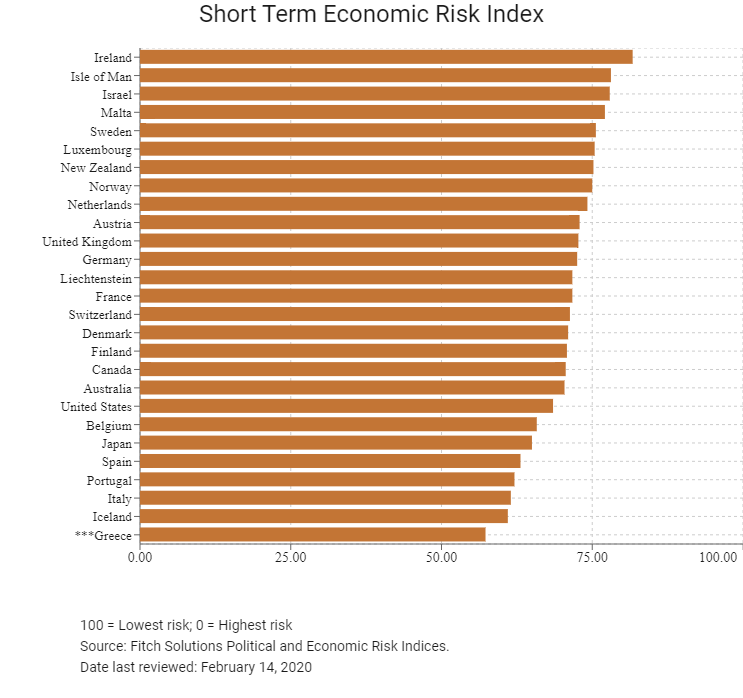

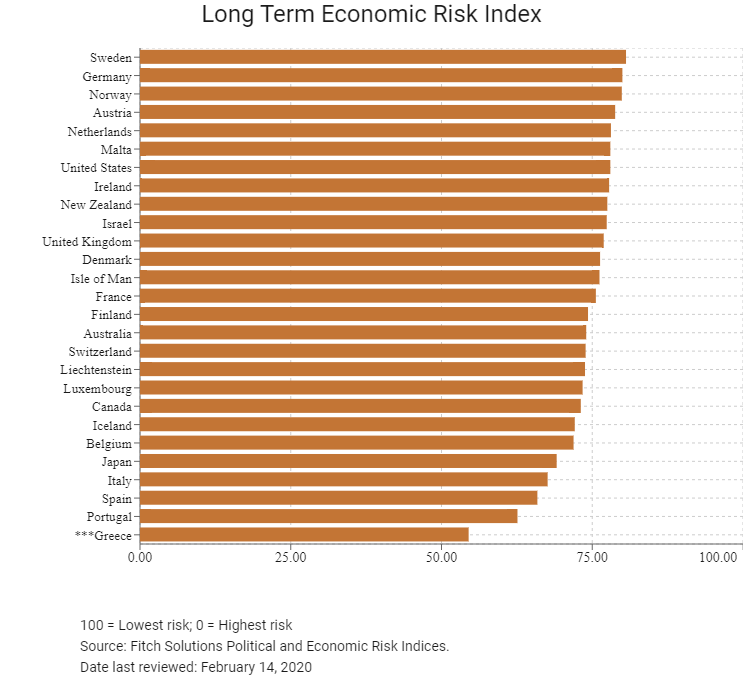

| Economic Risk Index Rank | 82/202 | 95/201 | 80/201 |

| Short-Term Economic Risk Score | 55.6 | 56.5 | 57.3 |

| Long-Term Economic Risk Score | 54.6 | 52.6 | 54.5 |

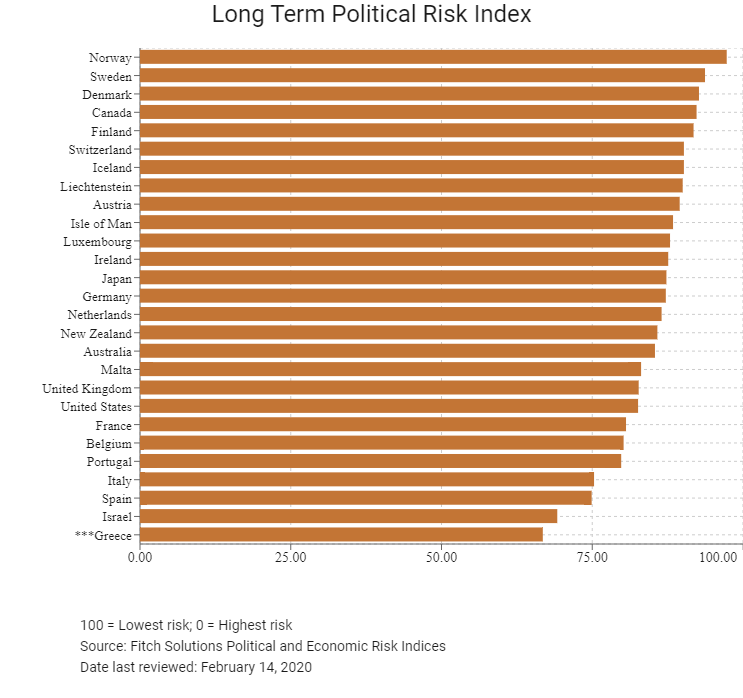

| Political Risk Index Rank | 81/202 | 81/201 | 80/201 |

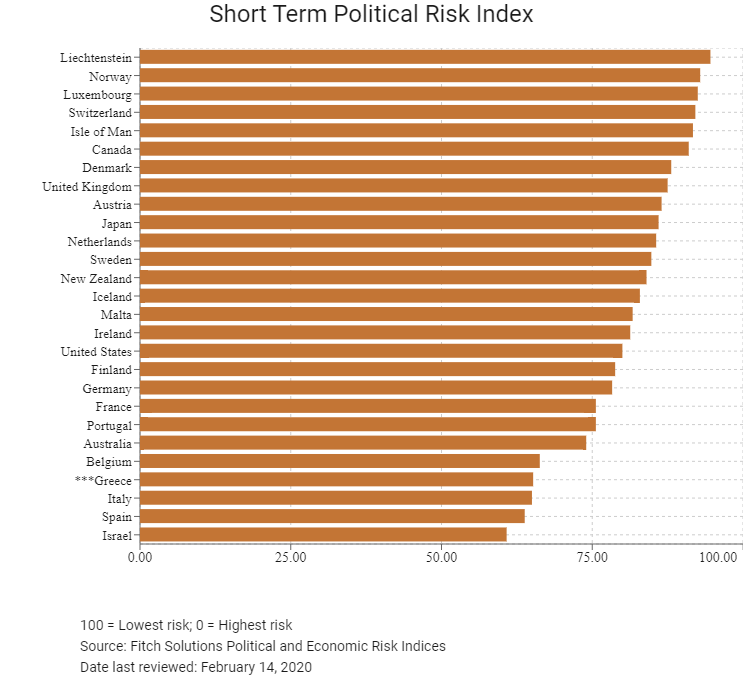

| Short-Term Political Risk Score | 61.0 | 65.2 | 65.2 |

| Long-Term Political Risk Score | 66.8 | 66.8 | 66.8 |

| Operational Risk Index Rank | 60/201 | 62/201 | 62/201 |

| Operational Risk Score | 58.2 | 58.2 | 58.0 |

Source: Fitch Solutions

Date last reviewed: February 14, 2020

Fitch Solutions Risk Summary

ECONOMIC RISK

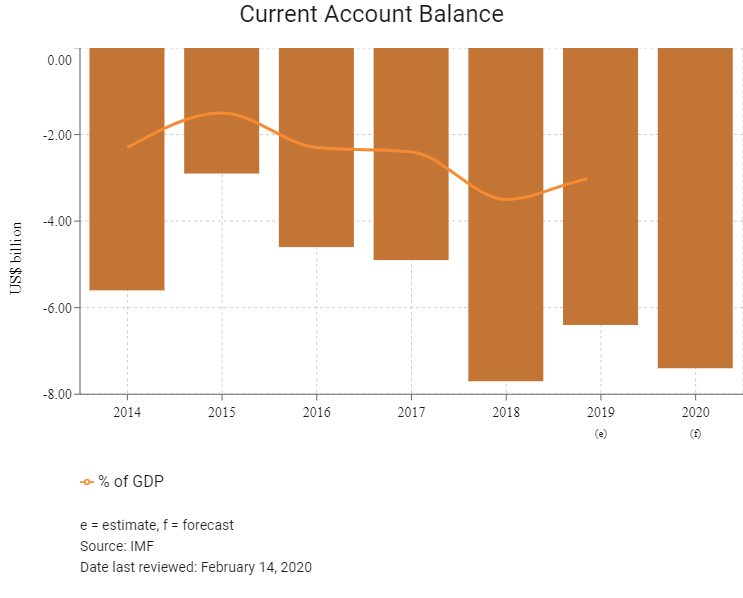

With Greece's creditors still to agree on significant debt relief, a banking sector still struggling with non-performing loans and a government tied to primary budget surplus targets, Greece's growth outlook is subdued for the coming quarters. The economy remains around 20% smaller than it was pre-crisis, implying the marginal positive growth rates over the coming years will be insufficient to drag living standards back to 2008 levels. A moderation of eurozone growth, increased competition from rival tourist destinations, the country's still high public debt levels and global trade slowdown pose risks to the tepid growth outlook. Domestic demand is likely to remain underwhelming, as unemployment continues to stifle spending. However, pro-business reforms from the current administration will provide some resistance to prevailing headwinds. Meanwhile, Greece will run a historically narrow current account deficit for the next few years, reducing previously systemic risks posed to macroeconomic stability from its large external imbalances.

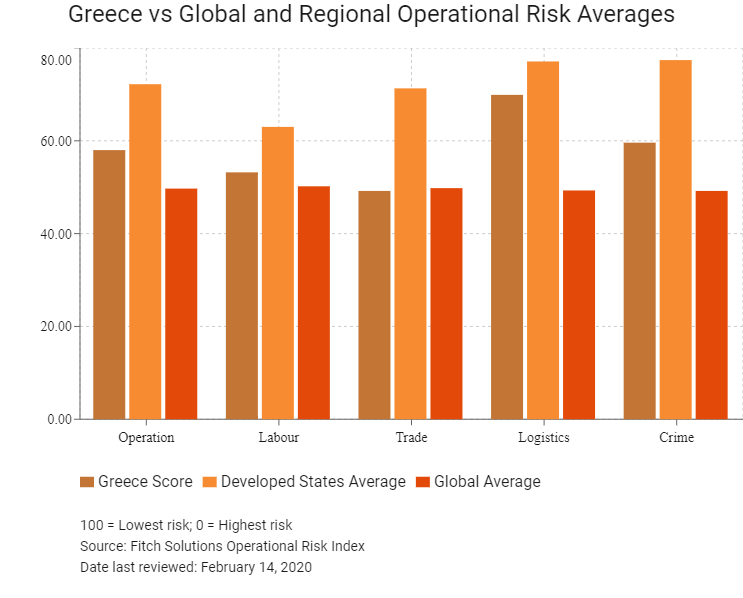

OPERATIONAL RISK

Greece offers a competitively educated labour pool and a transport network that facilitates trade and travel. The country’s trade bureaucracy is relatively good and streamlined and crime rates are low. Greece has high levels of unemployment, which provides potential employers with more ample recruitment options in the medium term. The high cost of employment, however, will remain a hurdle for businesses – particularly in labour-intensive industries.

Source: Fitch Solutions

Data last reviewed: February 17, 2020

Fitch Solutions Political and Economic Risk Indices

Fitch Solutions Operational Risk Index

Operational Risk | Labour Market Risk | Trade and Investment Risk | Logistics Risk | Crime and Security Risk | |

| Greece Score | 58.0 | 53.2 | 49.2 | 69.9 | 59.6 |

| Developed States Average | 72.2 | 63.0 | 71.3 | 77.1 | 77.4 |

| Developed States Position (out of 27) | 27 | 24 | 27 | 23 | 27 |

| Global Average | 49.7 | 50.2 | 49.8 | 49.3 | 49.2 |

| Global Position (out of 201) | 62 | 81 | 105 | 38 | 60 |

100 = Lowest risk; 0 = Highest risk

Source: Fitch Solutions Operational Risk Index

Country | Operational Risk Index | Labour Market Risk Index | Trade and Investment Risk Index | Logistics Risk Index | Crime and Security Risk Index |

| Denmark | 79.4 | 70.5 | 76.2 | 88.5 | 82.3 |

| Switzerland | 78.6 | 74.4 | 77.6 | 79.3 | 83.2 |

| Netherlands | 78.3 | 65.4 | 78.2 | 88.8 | 80.7 |

| Sweden | 77.6 | 66.8 | 78.1 | 86.7 | 78.6 |

| United States | 77.6 | 79.7 | 75.3 | 85.9 | 69.3 |

| New Zealand | 77.2 | 72.0 | 75.7 | 73.0 | 88.3 |

| Canada | 76.4 | 73.6 | 75.4 | 75.1 | 81.6 |

| United Kingdom | 76.4 | 70.2 | 79.0 | 78.3 | 78.2 |

| Norway | 76.3 | 63.8 | 72.2 | 81.2 | 87.9 |

| Austria | 74.7 | 61.9 | 71.9 | 83.6 | 81.5 |

| Finland | 74.4 | 54.9 | 74.1 | 84.7 | 83.7 |

| Ireland | 73.5 | 66.6 | 78.0 | 70.4 | 79.0 |

| Luxembourg | 73.4 | 54.3 | 77.6 | 82.5 | 79.3 |

| Germany | 72.4 | 66.1 | 69.0 | 80.8 | 73.6 |

| Australia | 72.3 | 68.7 | 72.1 | 68.4 | 79.9 |

| France | 71.8 | 60.7 | 71.1 | 82.6 | 72.8 |

| Spain | 71.6 | 61.0 | 68.9 | 80.6 | 76.0 |

| Iceland | 71.3 | 59.8 | 67.2 | 70.0 | 88.1 |

| Japan | 71.1 | 69.9 | 65.5 | 77.5 | 71.5 |

| Belgium | 70.8 | 57.1 | 72.8 | 82.3 | 71.1 |

| Portugal | 69.8 | 52.5 | 66.5 | 81.7 | 78.4 |

| Liechtenstein | 68.4 | 47.0 | 78.1 | 65.1 | 83.2 |

| Israel | 67.2 | 71.3 | 64.6 | 70.2 | 62.7 |

| Malta | 65.0 | 54.3 | 69.0 | 63.0 | 73.7 |

| Italy | 63.8 | 55.1 | 59.7 | 76.2 | 64.3 |

| Isle of Man | 62.8 | 49.9 | 62.4 | 56.6 | 82.4 |

| Greece | 58.0 | 53.2 | 49.2 | 69.9 | 59.6 |

| Regional Averages | 72.2 | 63.0 | 71.3 | 77.1 | 77.4 |

| Emerging Markets Averages | 46.2 | 48.2 | 46.5 | 45.0 | 44.9 |

| Global Markets Averages | 49.7 | 50.2 | 49.8 | 49.3 | 49.2 |

100 = Lowest risk; 0 = Highest risk

Source: Fitch Solutions Operational Risk Index

Date last reviewed: February 14, 2020

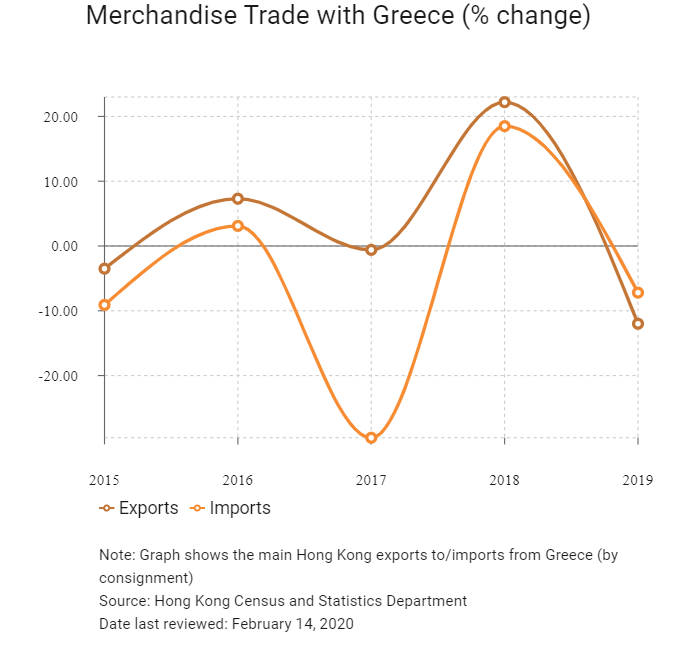

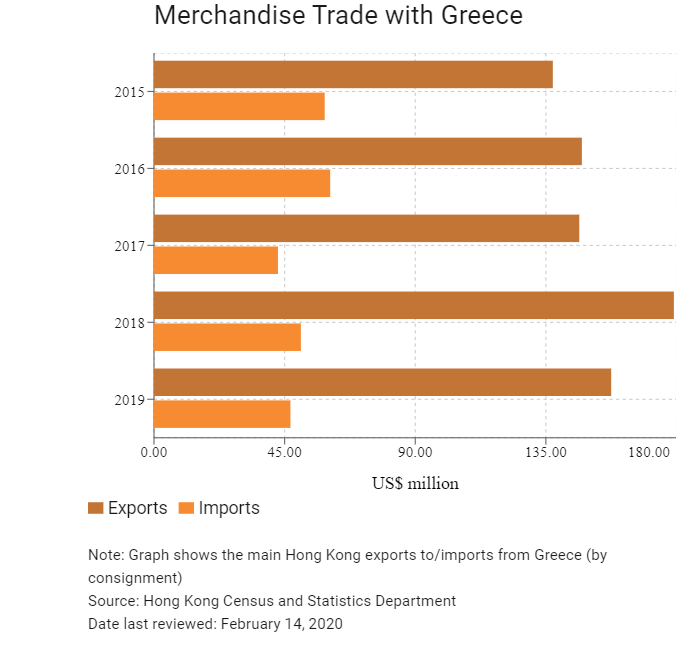

Hong Kong’s Trade with Greece

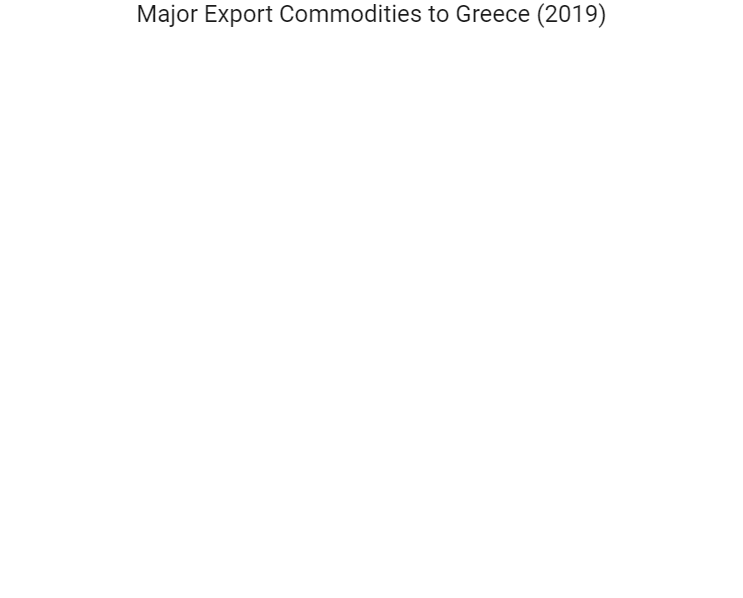

Export Commodity | Commodity Detail | Value (US$ million) |

Commodity 1 | Telecommunications and sound recording and reproducing apparatus and equipment | 83.2 |

Commodity 2 | Office machines and automatic data processing machines | 16.0 |

Commodity 3 | Miscellaneous manufactured articles | 16.0 |

Commodity 4 | Electrical machinery, apparatus and appliances, and electrical parts thereof | 13.9 |

Commodity 5 | Photographic apparatus, equipment and supplies and optical goods; watches and clocks | 8.2 |

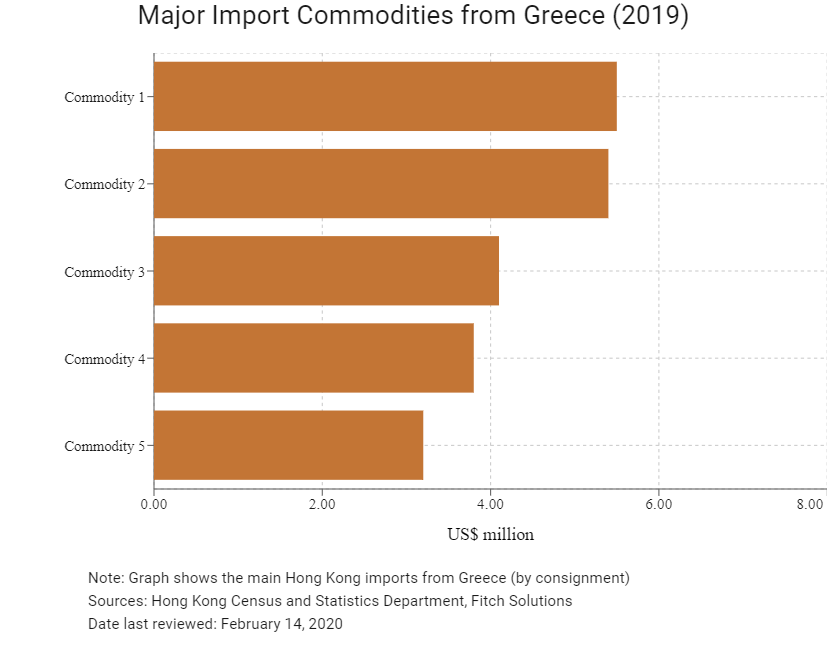

Import Commodity | Commodity Detail | Value (US$ million) |

| Commodity 1 | Photographic apparatus, equipment and supplies and optical goods; watches and clocks | 5.5 |

| Commodity 2 | Essential oils and resinoids and perfume materials; toilet, polishing and cleansing preparations | 5.4 |

| Commodity 3 | Road vehicles (including air-cushion vehicles) | 4.1 |

| Commodity 4 | Fish, crustaceans, molluscs and aquatic invertebrates, and preparations thereof | 3.8 |

| Commodity 5 | Vegetables and fruit | 3.2 |

Exchange Rate HK$/US$, average

7.75 (2014)

7.75 (2015)

7.76 (2016)

7.79 (2017)

7.83 (2018)

7.77 (2019)

2019 | Growth rate (%) | |

| Number of Greek residents visiting Hong Kong | 8,864 | -7.2 |

| Number of European residents visiting Hong Kong | 1,747,763 | -10.9 |

Source: Hong Kong Tourism Board

2019 | Growth rate (%) | |

| Number of developed states citizens residing in Hong Kong | 83,786 | 29.6 |

Source: United Nations Department of Economic and Social Affairs – Population Division

Note: Growth rate is from 2015 to 2019. No UN data available for intermediate years.

Date last reviewed: February 14, 2020

Commercial Presence in Hong Kong

2018 | Growth rate (%) | |

| Number of Greek companies in Hong Kong | N/A | N/A |

| - Regional headquarters | ||

| - Regional offices | ||

| - Local offices |

Treaties and agreements between Hong Kong and Greece

Greece and Mainland China have a double taxation agreement in place. The agreement was signed in 2002 and has been in force since 2006.

Source: ChinaTax.gov

Chamber of Commerce (or Related Organisation) in Hong Kong

The European Chamber of Commerce in Hong Kong

Address: Room 1302, 13/F, 168 Queen's Road Central, Central, Hong Kong

Email: info@eurocham.com.hk

Tel: (852) 2511 5133

Fax: (852) 2511 6833

Source: The European Chamber of Commerce in Hong Kong

The European Chamber of Commerce in Hong Kong

Consulate General of Greece in Hong Kong

Address: Room 1208, 12/F, 39 Gloucester Road, Wan Chai, Hong Kong

Email: grgencon.cg@mfa.gr

Tel: (852) 2774 1682

Fax: (852) 2705 9796

Visa Requirements for Hong Kong Residents

HKSAR passport holders can travel to the Schengen Zone without a visa. They can travel for tourism and business purposes and remain in the region for a period of up to 90 days.

Source: Visa on Demand

Date last reviewed: February 14, 2020